After the basic recording of daily business transactions takes place, this information needs to be summarized in order for it to be of any material use for the users of such information. These users mainly include the management of the business itself, so that it can evaluate the overall performance of the company's operations during a particular period. Other users include potential investors, the current shareholders, taxation authorities and other regulatory bodies.

All the journalized transactions are put under various distinct heads. For instance, if electricity expense is being incurred then it will be put under the head Electricity. And each electricity bill which is paid during the period will fall under this head.

The same is done for each and every head of the business. At the end of period these heads are balanced to determine, the credit or debit balance of the head.

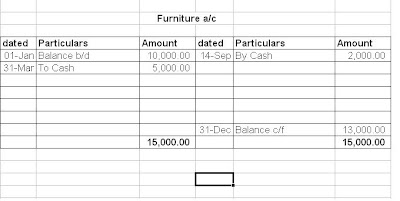

Below the Furniture account is shown for the year with basic entries during the year, and finally the account is totalled to determine the balance.

From this example of the Furniture account, the simple concept of posting entries related to Furniture into its respective ledger can be understood. The first item shown is the balance of Furniture which was available at the beginning of the period Jan-1. Then on 31-Mar new furniture was purchased for cash. This is shown on the right side of the ledger which represents the debit side. We know from past experience that an increase in an asset is debited.

Then, some of the furniture was sold for cash on 14-Sep. This will be represented on the credit side of the account as the asset is decreasing or going out of the business. At the close of the period, the account is totalled. This is done by adding all items on the heavier side of the ledger which in this case is the Debit side. After this total is achieved the items on the other side are simply subtracted from it. This closing balance is the figure which will be shown on the balance sheet.